Yes. Standard consolidation rules require that a U.S. affiliate must file on a fully consolidated domestic U.S. basis, including in the full consolidation all U.S. business enterprises proceeding down each ownership chain whose voting securities are more than 50% owned by the U.S. business enterprise above. The fully consolidated entity is considered one U.S. affiliate.

Do not consolidate foreign subsidiaries, branches, operations or investments no matter what the percentage ownership. Include foreign holdings owned 20% or more using the equity method of accounting. DO NOT report employment, land, and other property, plant and equipment and DO NOT eliminate intercompany accounts for holdings reported using the equity method.

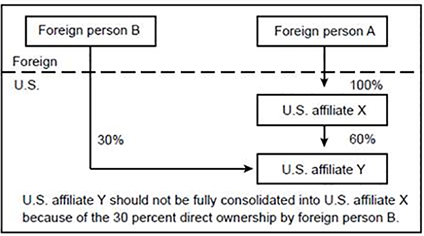

Exception 1: If a U.S. affiliate has both a direct and indirect ownership interest of greater than 10% that are held by different foreign persons, this U.S. affiliate must file its own BE-12. It should not be consolidated on the BE-12 report of another U.S. affiliate. See diagram below.

Exception 2: U.S. affiliates that are limited partners or that have an ownership interest in a U.S. limited partnership must follow the consolidation rules detailed at: www.bea.gov/help/faq/970