GDP by Industry

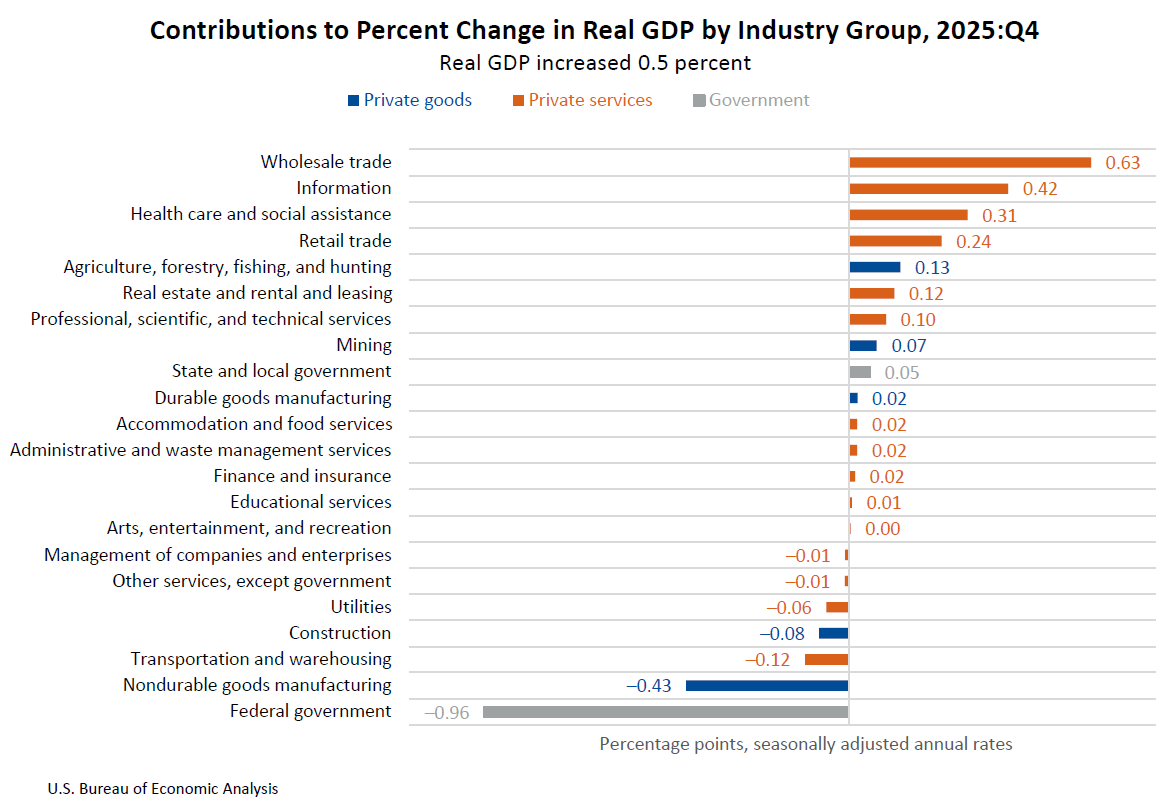

In the fourth quarter of 2025 (October, November, and December), the increase in real gross domestic product (GDP) reflected an increase of 2.3 percent in real value added for private services-producing industries that was partly offset by decreases of 7.8 percent in government and 1.8 percent in private goods-producing industries. Overall, real GDP increased at an annual rate of 0.5 percent in the fourth quarter of 2025 according to the third estimate released by the U.S. Bureau of Economic Analysis.

Note: GDP by industry statistics are released with the third estimate of GDP each quarter.

Current release: April 9, 2026 | Next release: June 25, 2026

- Data Archive HTML?HMI=3 Previously published estimates contain historical data and have since been revised

What is GDP by Industry?

An industry-by-industry breakdown of gross domestic product. In addition to showing each industry’s contribution to the U.S. economy, known as its value added, these statistics include industries’ compensation of employees, gross operating surplus, and taxes.

Contact Personnel

-

GDPLisa Mataloni

-

GDP by IndustryThomas Howells

-

MediaConnie O’Connell