Personal Income by State, 4th Quarter 2022

March 31, 2023

This technical note provides background information on the estimates of state refundable tax credits included in the third and fourth quarter of 2022 state personal income. The complete set of estimates are available on the Bureau of Economic Analysis (BEA) website; a brief summary of highlights is also posted on the website.

State refundable tax credits impact on third- and fourth-quarter 2022 state personal income

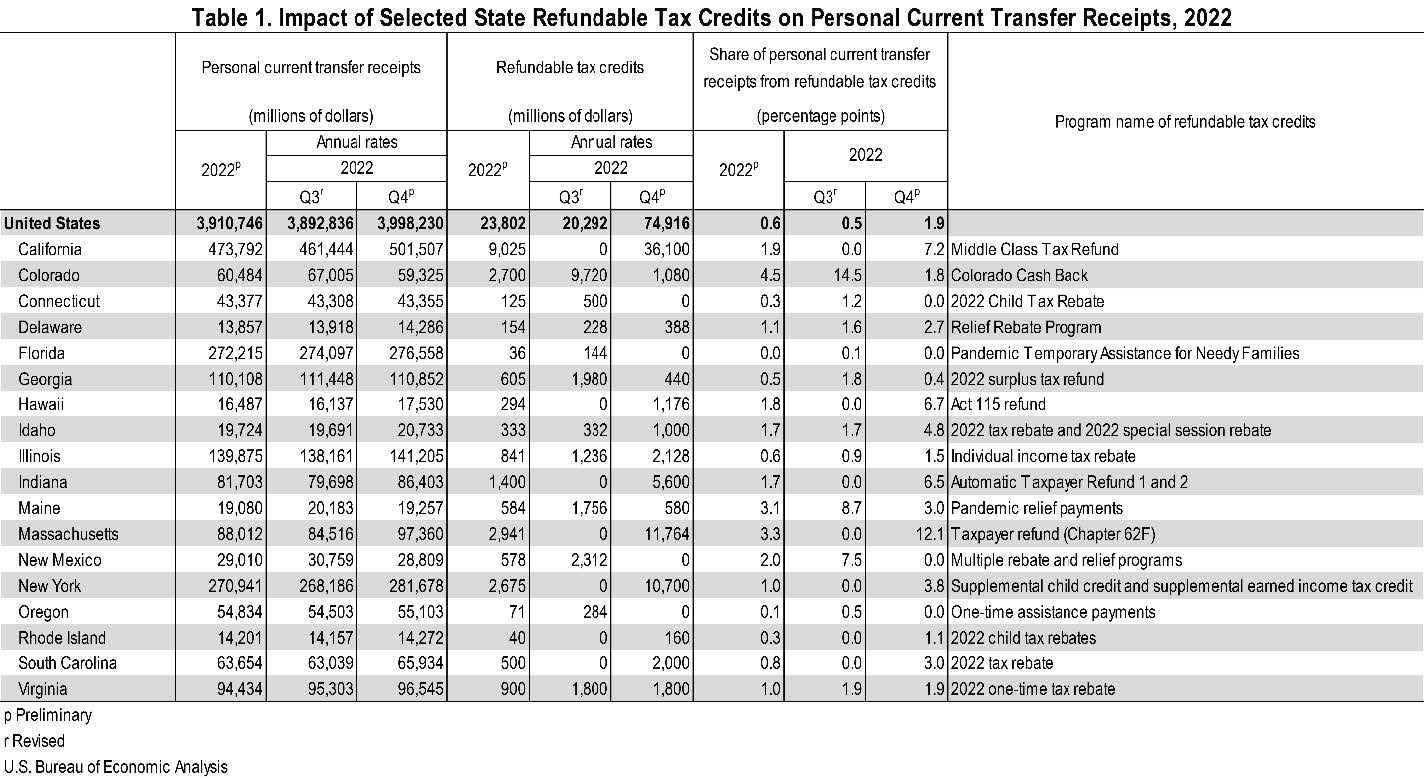

In the latter half of 2022, several state governments provided relief to the residents of their states by way of one-time refundable tax credits. Refundable tax credits typically allow taxpayers who meet certain eligibility criteria to reduce the amount they are required to pay in income taxes, and if the credits exceed the taxpayer's total tax liability, the excess is paid to them as a refund. Some states chose to distribute the full amount of these credits directly to individuals during the last half of 2022.

Data typically are not available to estimate separately the value of refundable tax credits that are regularly offered by state governments. The value of these tax credits is therefore recorded only implicitly as a reduction in tax receipts and not in personal income. However, a combination of media reports and state-level administrative data were available to estimate the value of these one-time 2022 tax credits. As a result, BEA recorded them as an increase in government expenditures (specifically as government social benefits to persons or personal current transfer receipts), rather than as a reduction in government receipts. The total value of these credits is reflected in increases in the personal current transfer receipts component of personal income in the states affected.

For more information on refundable tax credits and their relation to the National Income and Product Accounts, see the FAQ “How are state refundable tax credits recorded in the National Income and Product Accounts (NIPAs)?”.

The scope and dollar value of the refundable tax credit programs varied across states. Nationally, these programs accounted for less than 2.0 percent of total personal current transfer receipts in the fourth quarter. However, they were particularly important in Massachusetts, California, Hawaii, Indiana, Idaho, New York, Maine, and South Carolina, accounting for between 12.1 and 3.0 percentage points of total of personal current transfer receipts in these states (table 1).