What is the relationship between BEA’s statistics of direct investment positions at historical cost, current cost, and market value?

BEA publishes statistics on the stock, or investment positions, of U.S. direct investment abroad and foreign direct investment in the United States according to three distinct valuation methodologies:

- historical cost (book value)

- current cost

- market value, the featured valuation in the International Investment Position (IIP)

Each set of position statistics presents the value of these stocks based on different approaches to measuring the cost to the parent company of acquiring or disposing of them. IIP table 2.1 in BEA’s Interactive Data Application illustrates the three different valuation methodologies.

Direct investment asset and liability positions are composed of parents’ equity in, and debt with, its affiliates. Parents’ equity in affiliates includes parents’ holding of capital stock in, and capital contributions to, their affiliates as well as parents’ equity in the retained earnings of their affiliates. Parents’ debt with their affiliates, also called intercompany debt, consists of trade accounts and trade notes payable, other current liabilities, and long-term debt owed. In all three valuation approaches, debt is presented at historical cost (book value). However, equity is revalued to both current cost and market value by adjusting the historical-cost equity positions. In accordance with international standards, BEA records all components of the IIP at current period prices, rather than at historical cost. While the current cost and market value both reflect current period prices and both measures may be appropriate for different circumstances, the market valuation method is the featured measure of direct investment in the U.S. IIP.

BEA’s surveys on direct investment collect information at historical cost (book value).1 Historical-cost valuation is the primary basis used for valuation in company accounting records and is thus the basis on which companies can most easily report data to BEA.2 Historical cost estimates are presented on lines 15-17 and 32-34 of IIP table 2.1.

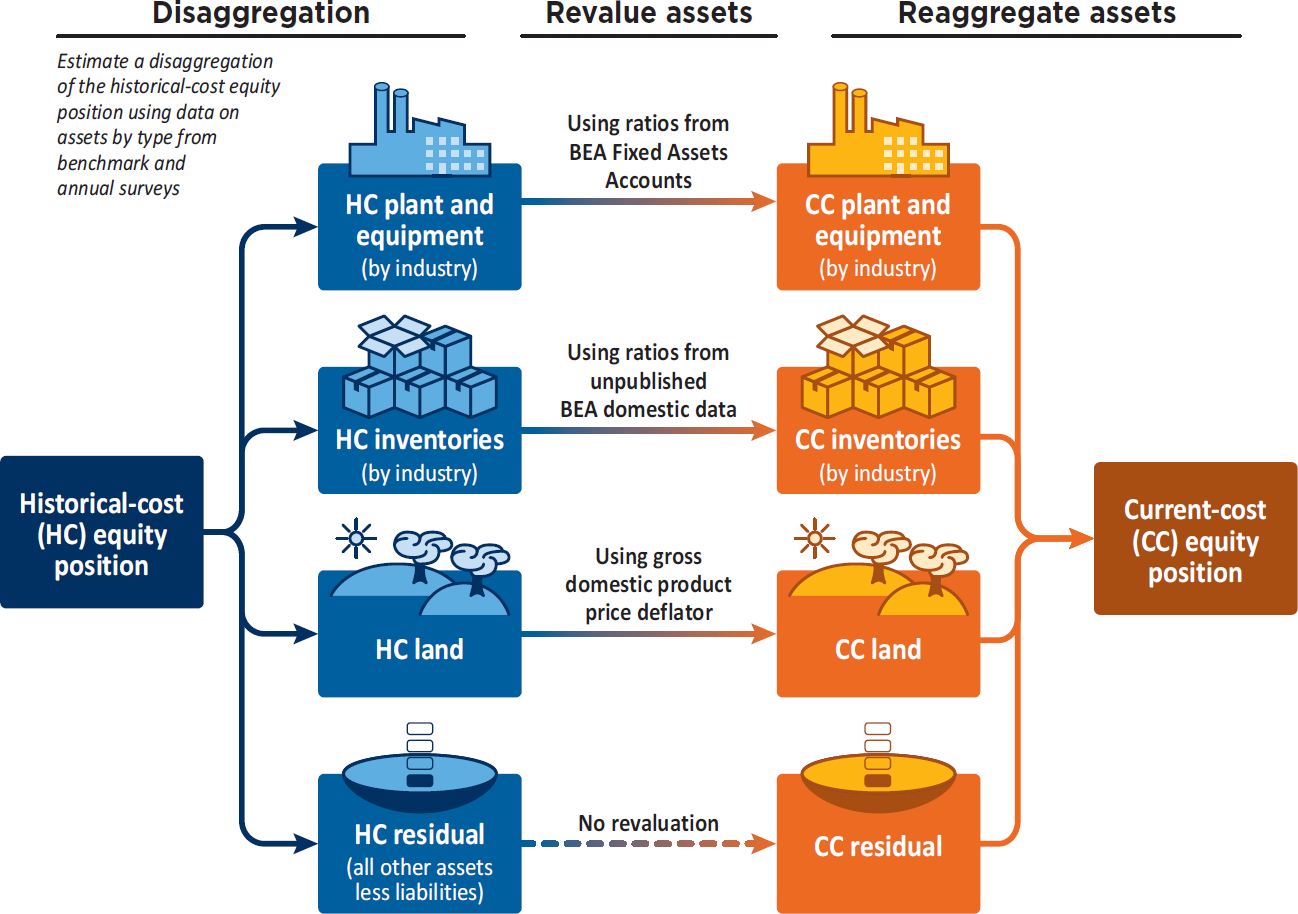

Current cost estimates revalue the equity claims parent companies have on their affiliates’ tangible assets from historical cost and reflect the cost parent companies would incur to replace these assets at current prices. Financial assets are not revalued, as values carried for these assets are assumed to be equal or approximate to their current-period values. Also, the estimates do not revalue mineral or other natural resource rights.

As illustrated in chart 1, the current-cost estimates revalue affiliates’ plant and equipment using ratios from a perpetual inventory model applied to domestic investment data, land using a U.S. gross domestic product price, and inventory stocks using estimates of current replacement cost. Current cost estimates are presented on lines 35-44 of IIP table 2.1.

Market value estimates revalue parents’ equity investment in their affiliates from historical cost (book value) to market value using stock market indexes to estimate the affiliates’ net worth, including both the current value of their tangible assets as well as the market value of intangible assets. It also reflects changes in the general economic outlook, reflected by stock market prices, that may not be related to the prices of tangible assets. The market value estimates revalue only the equity portion of the direct investment position because it is assumed that there is no difference between market and book value for intercompany debt.

Direct investment abroad by U.S. companies (outward direct investment) is revalued using a weighted average of foreign stock market indexes from MSCI. Foreign direct investment in the United States (inward direct investment) is revalued using the S&P 500 stock market index. The market value method assumes that using general stock market price indexes produces, on average, a reasonable estimate of the aggregate value of the equity in affiliates in a country. The change in the market value position between periods equals financial transactions plus other changes in position attributable to price changes, exchange-rate changes, and changes in volume and valuation n.i.e. (not included elsewhere).3 The direct investment market value revaluation is presented under price changes. Because reinvested earnings are included in direct investment financial transactions, the revaluation methodology excludes movements in stock prices attributed to the reinvestment of earnings to avoid double-counting. Market value estimates are featured in the net IIP and are presented on IIP tables 1.1, 1.2, 1.3, 2.1, and 2.2.

Additional information on how direct investment positions are presented in the International Investment Position (IIP) Accounts is available in chapter 23 of the International Economic Accounts: Concepts and Methods. PDF

[2] - Market values are often not available for direct investment because the equity for many direct investment enterprises is not listed on stock exchanges.

[3] - IIP Table 1.3 in BEA’s Interactive Data Application presents the integrated IIP.